With the virus having suspended football, this seems like a good moment to finally sit down and look at exactly how “rich” Tottenham Hotspur is as a football club, and therefore think about the question of how much we can afford to spend.

The Swiss Ramble recently performed its annual analysis of Spurs’ finances, and it is an exercise I like and admire very much since it attempts to put into perspective the club’s performance and context amongst the elite. Yet it has a major limitation, which is that it focuses almost exclusively on “profitability”, as this excerpt shows:

Source: Swiss Ramble twitter account

The problem, of course, is that profitability tells us very little about cash available, since the items on the P&L (including the profits after taxes) are mostly not real cash items. Instead they are filled with such concepts as depreciation and the gains recognized on the sale of players as assets. Essentially, these are accounting items. And I find it a dangerous way to look at a football club because it raises false expectations about how “rich” we are and therefore how much we should be able to pay for transfers.

I prefer to apply a financial perspective by looking at football clubs as one would any other business, through the company’s balance sheet and cashflow statements. The balance sheet gives us a sense of how indebted the company might be. But more importantly I like to look at the cashflow statement for a few reasons:

- Real cash items – the cashflow statement gets rid of non-cash items such as depreciation and replaces it with real cash such as capex

- Transfers – it more accurately captures the actual money going in and out on transfers including all hidden costs as well as payments spread over time – a £60m fee paid over three years should be seen as such and not lumped into one number

- Stadium investment – it captures all hidden costs but also allows for financing raised against the project, ending the “the stadium pays for itself” speculation.

Helpfully most financial accounts break down transfer spending in quite some detail, which in turn allows for me to get to my core concept: the pre-transfer free cashflow (“PTFCF”). For this I take the net cash inflow / outflow, and add back transfer spending which I assume to be discretionary. This brings us to a calculation which tells us how much “spare” money we would have available to spend in a given year, if we had wanted to.

Taking the June 2019 figures, this metric then allows us to judge – somewhat – our performance in the transfer window.

Pre-Transfer Free Cashflow by club for year ended June 2019 (£m)

We can see from this analysis that Tottenham came a fair way off Man Utd, Chelsea and Liverpool (and one assumes Man City, who do not publish a cashflow statement or give any notes to their Intangible Fixed Asset investments). Arsenal were the big losers of last year given their Europa League participation, and Chelsea show themselves as doing well despite not qualifying for the Champions’ League. To be clear, generating a negative cashflow (just like generating a loss) does not mean you have no money to spend; only that you must do so unsustainably out of your “savings”, which will show up on the net debt (which we will get to).

If we look at the year prior, this becomes even more stark, and highlights the fact that Tottenham, contrary to some assertions, was under real financial pressure during the stadium building process starting in 2017.

Pre-Transfer Free Cashflow by club for year ended June 2018 vs net transfer investment for the following year (£m)

Note: Since transfer spending runs July-June and mostly occurs during the summer transfer window, a June 2018 year ending is best contrasted with the June 2019 transfer spending.

At this point, Spurs were actually incurring a substantial negative PTFCF due to stadium costs, not least since much expenditure for large capital projects is paid up-front, for land acquisition and so on. Man Utd and Chelsea spent far more than they were generating – one might say generously, “investing for the future”; Liverpool were spending about as much as they might expect; and only Arsenal were spending significantly below their capacity, buoyed no doubt by the knowledge that they were not in the Champions’ League. Indeed Tottenham’s tiny net expenditure of ~£3m was quite flattering under the circumstances.

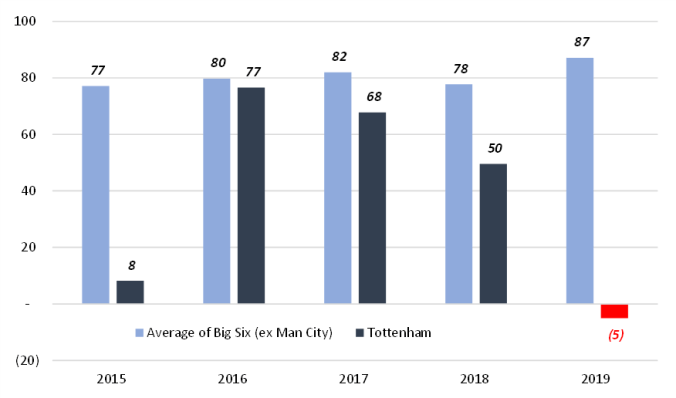

In fact, if we look at how Tottenham have performed on average against the rest of the Top Six (excluding Man City), we have had a tenuous few years.

Three-year rolling average Pre-Transfer Free Cashflow (£m)

On a rolling three-year average, the other clubs have managed a PTFCF of around £80m per year over the last five years, whereas Tottenham, having clawed our way into contention by 2016, have actually seen the gap widen again in the subsequent years. In other words, we really are not that well-off, are some way behind the other Big Six teams, and cannot spend the money on transfers that some fans seem to believe we now should. The stadium remains a massive gamble and has to succeed as a standalone business for us to begin making up the difference with the other clubs.

To cap things off, let us just look at the “savings”. A net debt position is typical of most companies and football clubs are no exception. Furthermore, the ratio of that debt to net assets or ‘shareholders’ funds” shows the relative indebtedness of a business.

Top Six clubs net debt (£m) and gearing for year ended June 2019

On both measures, Tottenham are more precarious than our peers. Not only is net debt larger in absolute terms, carrying with it the funding for the stadium; but alone amongst the Big Six, our gearing is at more than 100%. No doubt much of the stadium borrowing is ring-fenced to a degree, and probably operates on a project finance basis; nonetheless the cost of the debt will weigh Spurs down through interest payments for some time – and the analysis gives a sense of how much better off Man Utd really are than us, for instance. Daniel Levy, who is no stranger to this situation, will clearly not be minded to let spending get out of hand.

Some of this will be well-known and obvious to observers. The reason I raise it is the danger of football fans demanding spending beyond what is possible – and Spurs have been particularly under the microscope for this. The Swiss Ramble’s analysis – whilst perfectly legitimate and technically correct – conveys a very misleading impression over our financial clout. Headlines about record revenues and profits on the P&L, lead to questions (from those who should know better) of “where has all that money gone?”. In the end, Spurs just are not yet that big a club, and whilst I am confident that we will reach our goals, it will still take some time before we can splash out.

**************************************

Browsing the internet after posting, I came across the University of Liverpool’s football finances website, which has recently just posted about Premier League club values for 2018-2019, which, whilst doing some equally interesting things, has rather fallen rather into the same trap. Their proprietary “Markham Multivariate Model” is based on net profit adjusted for one-off items, but unadjusted for non-cash items. The formula is quite off-the-wall in other aspects too but I will let that lie for now.

Nonetheless it leads to what I think is just as unhelpful an output (below), saying:

Spurs overtook both Manchester clubs at the top of the table on the back of reaching the Champions League final, a fourth-place finish in the Premier League and a wage bill barely half that of Manchester United.

Even from the eyes of a purely financial investor, this cannot be true. Spurs’ true hidden value, if you want to see it this way, is the stadium value and its future earnings but as far as I can see this has not been captured by Markham. If you strip that out, however well managed our wage bill is, a DCF of Tottenham vs the other clubs would not come to this conclusion. My opinion: head in hands.