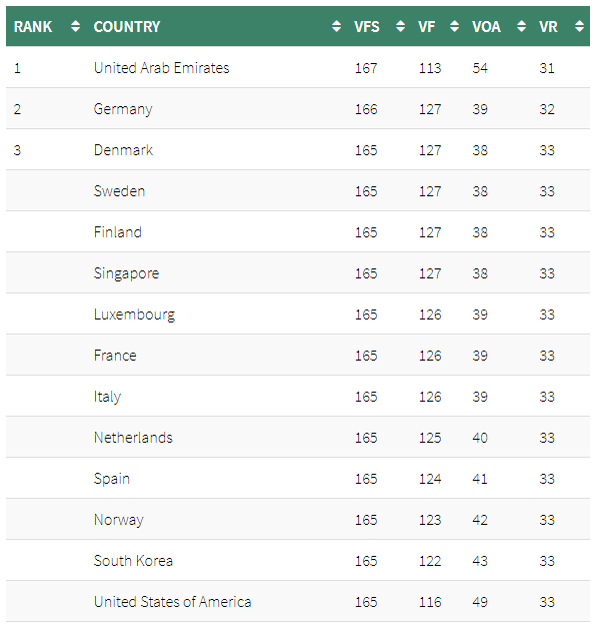

Various sets of passport rankings have recently come to my attention, for the most part offered by private wealth management firms discussing how best to migrate for asset protection. Looking at this carefully though reveals a great deal of lazy thinking which mostly show rankings like the following:

Source: Atlas & Boots 2019

This kind of assessment has become confused in recent years given the slow evolution from full visas to visas-on-arrival and electronic visas, as the above table demonstrates. For me, a visa-on-arrival satisfies the “get on a plane right now” rule, whereas electronic visas, whilst making life much easier, does not. Even without these nuances however, it should be obvious that the major problem with this simplistic ranking is that not all countries are of equal attraction, and the fact that one has visa-free access to Belize probably should not be considered on the same level as visa-free access to the European Union.

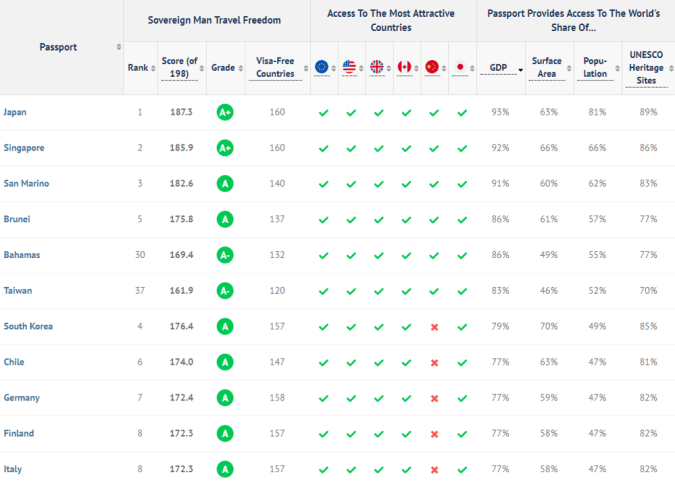

To combat this problem, a few more useful rankings have been created, looking at exposure to GDP and exposure to population for instance (a full overview of the various rankings can be found here). Both are useful in their way, but neither tell the full story. Of these various systems though, my preferred one is that created by Simon Black on his investment and thought blog The Sovereign Man (a great name, I must say) which basically uses a formula of 50% GDP and 50% “attractiveness” based on various things like UNESCO World Heritage sites and so on. This produces a rather different ranking and one which makes a lot more intuitive sense:

The heart of the matter, as can be seen in the central columns above, really revolves around who has access to both the US and China, of which there are very few. It is pretty clear that of non-tinpot countries, Japan and Singapore have the best passports by some distance and reflects the two countries’ substantial efforts to build the access network over the last few decades. Given their economic model, this does merit praise for the foresight and dedication – Japanese people are restricted only from Russia and some parts of the Middle East and Africa, with Brazil needing an e-visa. Altogether a very generous deal.

Japanese passport access as of 2018

Source: The Sovereign Man

Yet there is still an additional angle I would like to look at, which returns us to the “economic opportunities” component of such an analysis. Currently, a GDP-based ranking typically favours OECD passports since they have access to the US, the EU and Japan. But the problem is, this reflects the past, not the future: if you were a businessman, investor or entrepreneur today the historical economic clout of individual countries is not the important metric; rather it is the areas of future growth. To this end, I wanted to look at where global growth is coming from and the best proxy I have devised is that of the 5-year forward incremental GDP additions, as forecast by the IMF. In other words, how much more GDP is being added by each country over the next five years, in dollar terms. Furthermore, I also applied the IMF’s PPP adjustment to these, which as discussed previously on this blog, is I think a meaningful if imperfect way of looking at spending power. This is again relevant from the perspective of someone trying to understand where real economic opportunity might lie.

Therefore when looking at this “economic opportunity access”, a completely different picture begins to emerge. I do not have the resources to put all the numbers through for every nationality but below take a small sample to give an indication of my point:

Note: 5-year forward adjusted for PPP; e-visas (eg India) are weighted at 50% access

I have looked at just four passports (China and the US, Hong Kong and the UK); and looked at the access to the ten largest countries of future opportunity. In this analysis, Japan and Singapore would of course again come out on top since they have access to almost every country on the list. China and the US, as the largest economies, are included merely for benchmarking. But looking at third party countries one can see that Hong Kong maintains quite an advantage. The UK for instance represents most of those countries in the OECD which “side” with the US; whilst Hong Kong represents many of those who do not. Based on the top ten future economies, a Hong Kong passport holder has visa-free access to an additional US$7 trillion of GDP growth in the next five years compared to the UK. In many ways, it is positioned for the future like few others.

I will finish with the caveat about all this offered by Simon Black, and which applies to my analysis also:

The only goal behind The Sovereign Man Global Passport Ranking is to assess each passport’s quality as a travel document. We did not attempt to measure the merits of being a citizen in any country. This means we didn’t account for any country’s political stability, wealth of its citizens, freedom of press and speech, ease of doing business, or any other factors. And we didn’t account for the ability to move to another country with the passport. For example, Portugal’s passport didn’t get any additional points because Portuguese citizens can freely move to any other European Union country such as France or Germany. The goal of this project was to assess each passport’s quality as a travel document only.

Nonetheless, even with this caution I believe it is an important way to look at this passport analysis over which so many fight so fiercely. From a business perspective, not all economic access is the same.