The shenanigans of the Conservative Party gives me a moment for some fun: what if the Tories really did cast out another leader now, just a few weeks into her tenure?

First, I should emphasise that I do not predict at this point that Liz Truss will be removed. Nonetheless, neither do I think it completely unlikely, since MPs will grasp at almost anything which they think may help them get re-elected and, let’s be honest, nobody wants to face unemployment in this current environment.

So my logic is as follows:

Liz Truss may be deposed by MPs seeking to try and move on quickly from the current crisis (25% chance)

MPs will not give members a choice again, if this occurs. Instead, they will avoid the whole thing by presenting a single candidate as a fait accomplis (100% certain).

MPs will look to the past, not the future, when seeking their consensus candidate. With an election only two years away, I do not believe many will want to “try something new”, but rather look for a caretaker that minimises the damage from an election that seems almost certainly lost (70% likely).

There are only a few candidates suitable for this role, balancing out their status, past experience and willingness to serve. I believe only former PMs, Chancellors or high profile leadership candidates would be options. May is on obvious candidate (100% true).

There are really only a few names who can make this list. Boris is too recent and probably uninterested. Sunak and Javid, two former Chancellors, will both want to distance themselves from this irretrievable mess and believe they still have future careers. Several others, such as Hammond or Rory Stewart, are no longer MPs. To my mind, only three people would “do their duty” and lead in the current circumstances” Michael Gove, Jeremy Hunt and Theresa May.

So who knows what will happen? Gove seems too opportunist. Hunt might work but is a little faceless. I do think Theresa May has one quality, which is that she is dogged and hard-working and will provide some reassurance. Moreover, she has dealt almost entirely in crises. As a caretaker, there would be many worse. All this gives me the chance to return to one of my favourite memes:

The decline of Sterling in recent days has caused the kinds of panic amongst MPs and commentators usually reserved for global warming, Brexit and early England exits from finals tournaments. As an economist, I can testify that currency economics is amongst the more arcane and complex – at least, to model. What traders do on a whim may reflect current issues, or longer term ones; but precious few really know – certainly not politicians.

First, we should be clear about what the exchange rate is or is not. It is not, for instance, a broad measure of “a country’s strength”, a term that has been bandied around by gammons and globalists alike as they face the prospect of achingly expensive holiday costs to Mallorca and Miami, respectively. Nor does it reflect “how rich we are”, as though a 20% fall in the pound makes people, in any real sense, 20% poorer than they were weeks ago. Exchange rates are a measure of value, particularly for lubricating cross-border trade, and more than anything are a measure of demand for money and assets within an economy, from abroad.

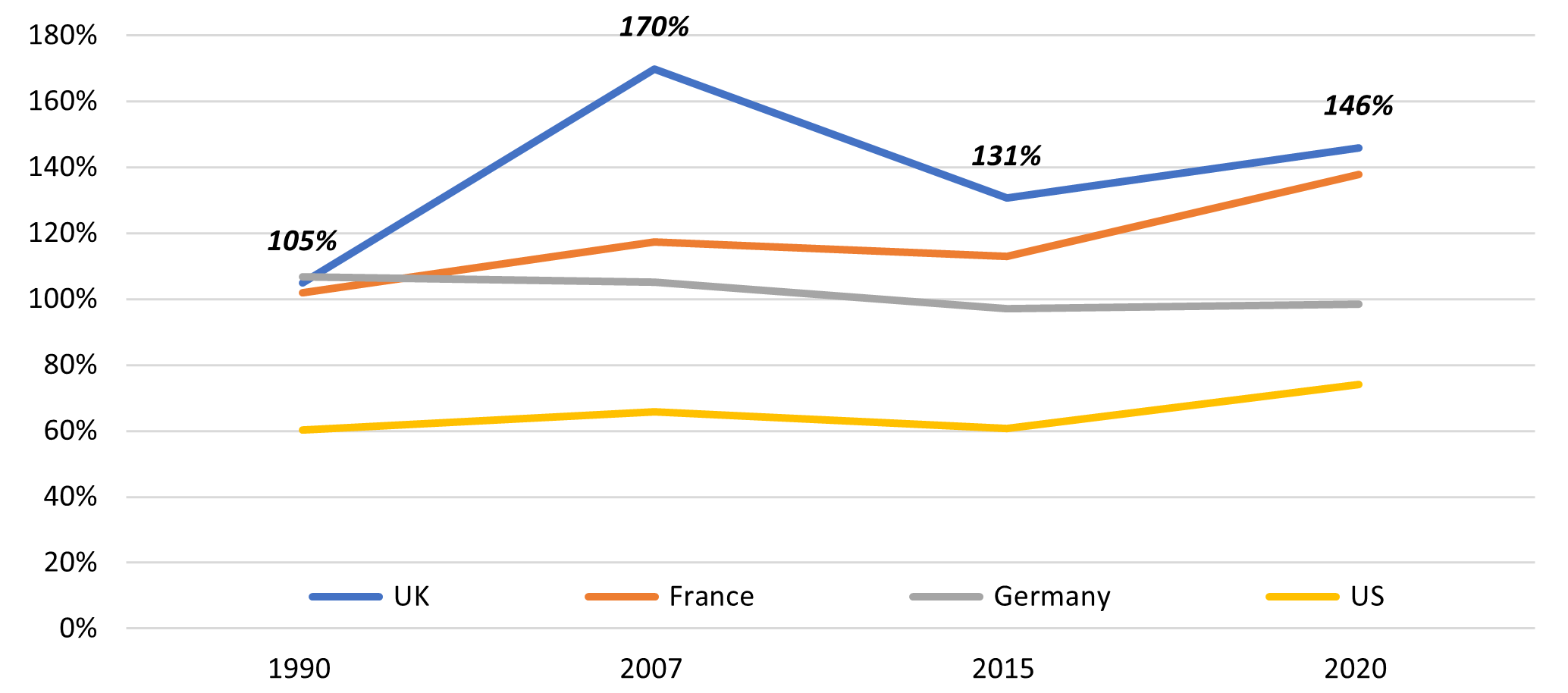

A strong economy can of course lead to a strong currency as people seek to invest into your country. Over time though, much of this will be ironed out through PPP as import prices start to rise over time reflecting demand. But currencies can also be artificially high, often for prolonged periods, due to trends such as the continued opening up of various asset classes to foreign capital, which can happen without the underlying economy producing anything more than it did before. I refer to this as the financialisation of an economy, a common feature throughout the Anglosphere from the 1990s onwards. Britain is particularly guilty, as seen below, and these numbers do not even reflect the unseen financial burden placed on UK taxpayers from housing foreign banks.

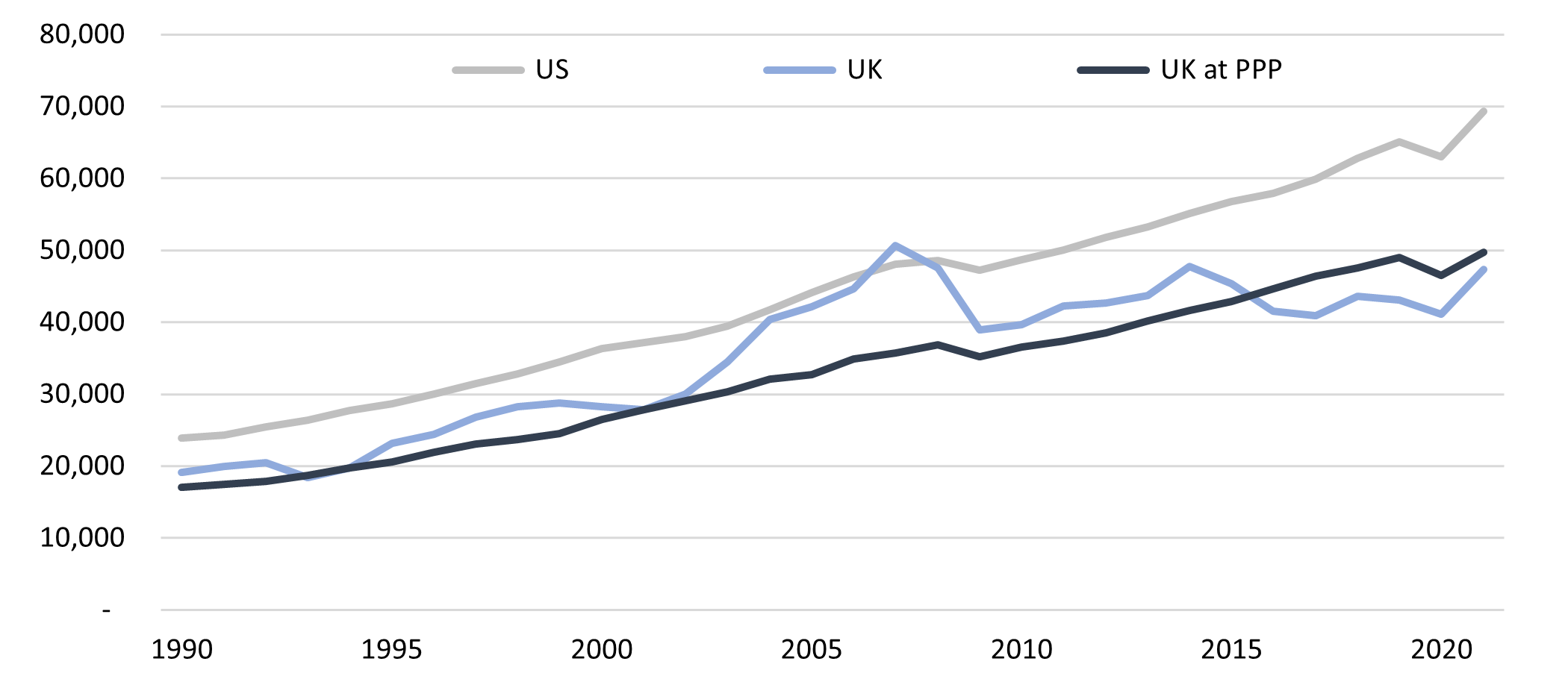

The consequence of all this is important: Sterling has been over-valued on a real economy basis for years – since well before Brexit or even the global financial crisis. The 2:1 exchange rate against the dollar reached in 2007, for instance, may be seen as the height of a monetary hubris unleashed by Thatcher but really bedded in by Gordon Brown, her true son. Everything was thrown into the financialisation of the economy and, as a second layer of back-up, the property market which saw Britons become richer by gross asset value but not usually by income or net assets. One way in which this washed through, therefore, was through looking at the gap between nominal exchange rates and PPP, where it could be seen that Britain was getting no richer compared to America than it had before or since. The yawning gap in the mid-2000s was totally driven by things other than the UK economy.

GDP per capita at PPP, US vs UK since 1990

Source: World Bank

In my humble opinion, something approaching parity between Sterling and the dollar had been due for a long while. I must admit to quite some surprise at how small the fall in Sterling was after the referendum in 2016, and had always assumed a rate of closer to 1.1-1.2 over the succeeding years. That it has taken a second crisis to cause the devaluation speaks more of the limited attention span and economic comprehension of currency traders, than it does of any lingering strength of the post-Brexit economy to punch above its weight.

The decline has now gone beyond my own instinct of where the “natural” level. This may be an exaggerated response to the budget from the markets, it may be my underestimation of British strength, or it may just be, like so much else, a temporary feature of the vagaries of the markets. On the other hand, it could signal a further long term deterioration of the structure of the UK economy. Either way, this decline had been coming for years and should have been expected. Even without Truss – indeed even without Brexit – we should have been at lower levels than what has been the case.

Because this “crisis” has really exposed how weak Britain had been for so long: continued poor productivity, an enormously skewed domestic economy with a whole political apparatus focused on maintaining house prices, and rampant financialisation to the detriment of the real economy. It is an unedifying sight to see semi-literate, over-reacting traders being observed and reflected by even less literate and even more hyperactive MPs and journalists. However more than anything, we should be digesting this new normal as the correct reflection of where we have been – and it may even help us plan properly going forward.