ASEAN is not a single place – there are winners and losers

Emerging markets have frequently been grouped together in the expectation that evolution in one could be carried across to others, and thereby allow investors in particular to draw large thematic lessons. The Asian Tigers was one example, BRIC was another; the Economist even spent an inordinate amount of time trying to find a successor to BRIC, all versions of which were unsatisfying. Southeast Asian economies are often put into one bucket, too, given what appears to be a similar stage of development between several of them, their proximity to the regional influences from Japan and China, and most of all due to the supposed progress of ASEAN.

However, taking a dispassionate view there is little reason to see these markets as similar enough to have a common investment principle. Indeed, I would argue that several of them face diverging fortunes and I very much like some of these markets and do not have time for others. There is a surprisingly limited amount of analysis from the outside on these markets individually; and when they are written, they are often quite amateurish.

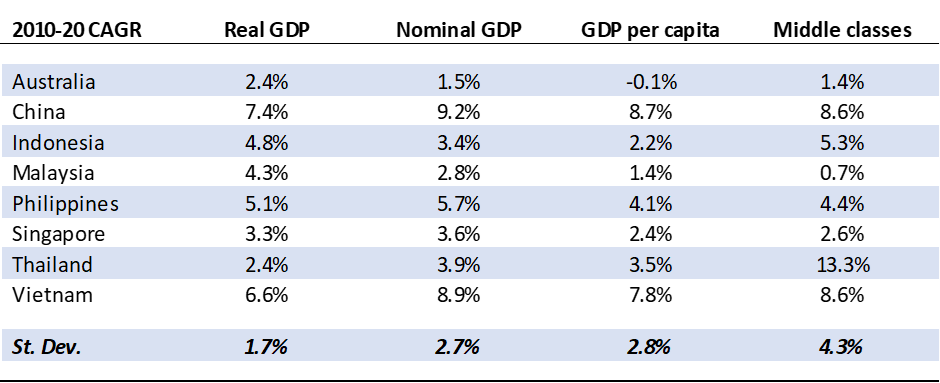

So let me get to who is Good and who is Bad in SE Asia. To begin with, it is worth looking at the macro numbers over recent times to consider which countries if any, have actually made progress. On the face of it, many in the region have performed decently compared to their OECD brethren. Yet ultimately the variation beyond real GDP, to which analysts are constantly beholden, shows quite a difference.

Note: “Middle classes” refers to population with greater than US$10,000 of wealth per capita; standard deviation calculation excludes Australia which is only included for comparative purposes

For a start, whilst real GDP numbers look somewhat comparable and almost clustered towards the 4%-6% range, this becomes markedly less so when looking at other metrics, and the standard deviation shows this. These others are important, too: we look at nominal GDP from an investment perspective because earnings and returns are nominal, not real. Per capita numbers wash out the effects of rapid population growth as an artificial bolster for underlying growth. Middle class population tell us how any of this notional growth is actually converting into mass consumers.

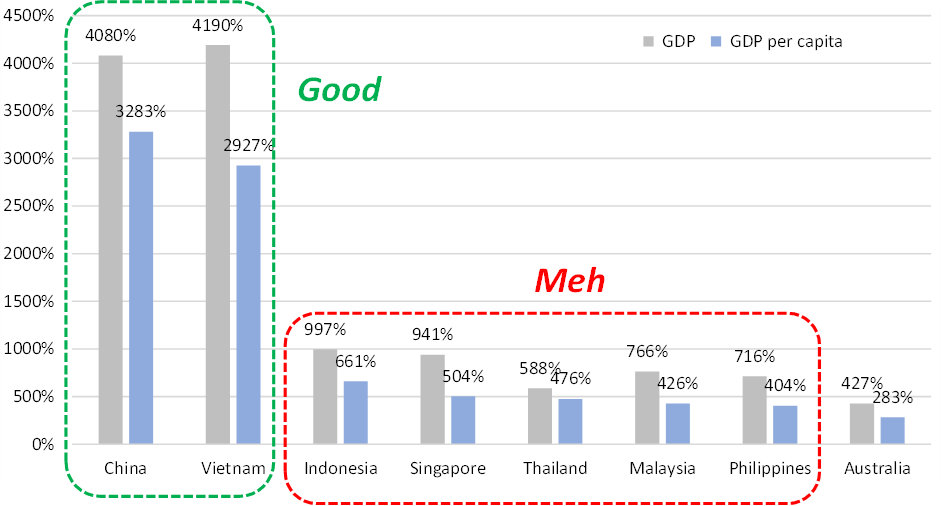

Much can be read into these figures but the most stark representation of it all, for me, is looking at total growth in recent years. Below is the total cumulative nominal GDP growth since 1990 for all the main countries in the region:

It turns out there are really only two groups of economies in emerging Asia: those that have generated huge amounts of growth and those which are just trundling along. China and Vietnam come from different bases but share the enormous benefits of a post-Communist economic surge; almost everyone else is unremarkable – both developed Singapore and Australia are not all that different to supposed stars such as Indonesia, Malaysia or the Philippines. China and Vietnam have performed not just better, but better by an order of magnitude.

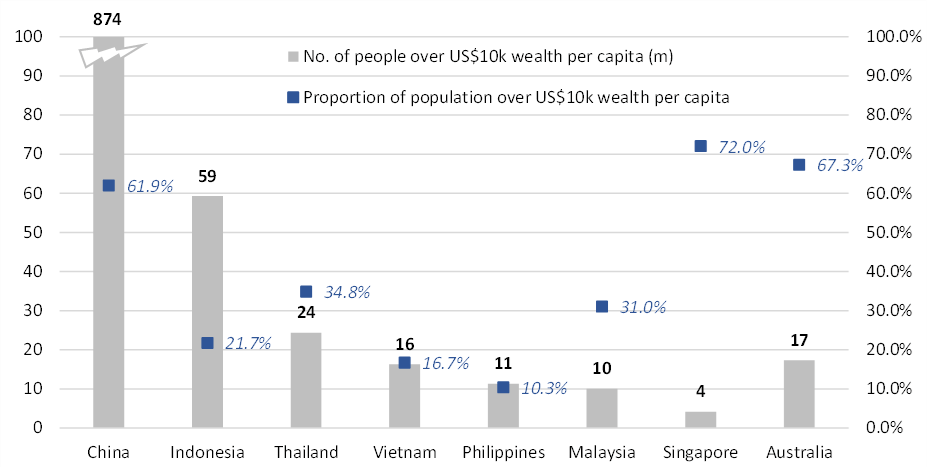

This has a knock-on effect on middle class consumption. Using the Credit Suisse data, I tend to look at the numbers of people who have US$10,000 in assets as a guide – what I call “true population”. China of course has created a huge true population who can and do consume – but elsewhere we can see why our views should be moderated. Indonesia, for instance, has 250m people; but only a fifth of them are real and – as per the table above – their track record of growing this has been poor compared to Vietnam for instance, which has a smaller true population but is growing it quickly.

I will delve more deeply into Indonesia and Vietnam in future posts, but the overall message here is clear: SE Asia is not a single type of market and there are clear winners and losers. The reasons why can be explored elsewhere but simply having a large population is not going to mean a country will develop within the time-frames we need to make money. Demographics is not destiny, and political and economic systems matter. Investors and companies ignore this at their peril.