Monetary unions rarely fall down on their economics, but do so rather on the political competencies of the participants

The reaction to this week’s announcement from our Argentine and Brazilian friends, of tentative plans for a monetary union, met with predictable – and mostly justified – derision. “This is insane“, tweeted Olivier Blanchard from that bastion of economic propriety, the IMF. Below the line comments on the FT included one wag which described this as “a version of the Euro where every member is Greece”. And no wonder, since the announcement was accompanied by the kind of hubris more befitting Argentina’s junta days than now – “It is Argentina and Brazil inviting the rest of the region” they said, as though they occupy anywhere near the global status of their erstwhile Brazilian partner these days.

Yet, this is consequently a poignant moment to reflect on currencies, economies and the lessons of the Euro – to date, the only effected currency union in existence (there are a few others, but these are paltry). There are in reality two main drivers of such things: one ‘imperial’, the other ‘democratic’.

The ‘Imperial’ model of monetary union is where the economics of one power dictate the others. Historically this includes arrangements such as the Sterling Area, but in today’s more consensual world it more regularly indicates some states wishing to copy or import the strengths of a neighbour. In the Euro, it was very apparent that the motivation for many countries was the ability to import Germany’s low inflation and depreciation – basically, to emulate and outsource the role of the Bundesbank. This was certainly true of Italy, and even if they do not admit it, the French. The Euro became (and is) and consensual imperial project on behalf of Berlin. I, for one, have no qualms at all about such a thing.

But the Euro, and its predecessor the ERM, was also conceived of as the other model, the ‘democratic’. In this world, the new currency would marry German manufacturing with French agriculture and British finance. This provided not only a balance, but also allowed the EU to exceed the sum of its parts – it relied on complementarity and relative equality. At that point, too, the only countries involved were wealthier ones, not the collection of rich and poor that it became. The problem was that over time, two truths emerged: Britain was too Eurosceptic to join the Project, and France was in fact nowhere near equal to Germany. Therefore, the ‘imperial’ model superseded the ‘democratic’.

This was aided by the fact that Germany, suffering from the after-effects of reunification, entered the final straight pre-Euro in an artificially depressed exchange rate. The best way of looking at this is through this exchange rate effect on current accounts over the period:

The reversion of this undervaluation over time inevitably led to German economic and monetary dominion over the rest of the Eurozone. Economic empire became a reality and, although there are plenty of high profile problems requiring German taxpayer bailouts of, say, Greece, this simply became the “cost of empire”, in exactly the same way the UK home population had to cover the balance sheet of the British Empire after the 1850s.

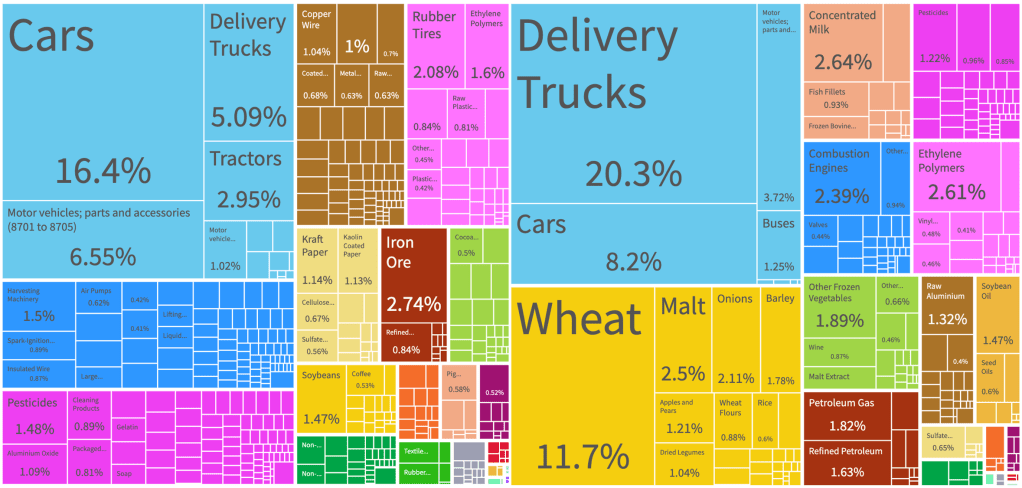

If we therefore look at the proposed Argentine-Brazilian ‘Sur’, we have to ask ourselves before we dismiss it, what are the objectives and how might they be achieved? The Argentina peso is a basket case, but the Brazilian real is not exactly the Deutschmark either. Regardless of recent crises therefore, the Sur must be based on some sort of complementarity: theoretically a commodity exporting superpower whose overwhelming dollar reliance might be transformed into a monetary of its own, aided by some flattening of the cycles between various commodity prices. The trade between the two countries, interestingly, is much more diverse than one might think:

Brazil exports by value to Argentina (left) and vice versa (right) in 2020

Now, none of this is to suggest the Sur will work. On the contrary, guessing today, it seems unlikely to ever take form. Neither Brazil or Argentina represent a clear imperial winner over the other. Neither is notably better managed (though Lusophile lobby would contend that Brazil has had a better recent innings). Yet neither are they clearly complementary: although Brazil is Argentina’s largest export destination, at just 14% this is not determinative; on the other hand Argentina accounts for just 4% of Brazil’s exports, dwarfed by its relationships with China and other emerging markets.

In fact, far from being different, Argentina and Brazil are probably too similar. Apart from a history of poor public policy, the strengths outlined above are their weaknesses too: both countries are still overly focused on commodity trade. Dollar-based raw materials account for two thirds of each country’s exports. Indeed logically, both might be better adopting the Dollar instead of looking at such a doctrinaire project – Argentina’s experiment with the peg over the 1990s, whilst it collapsed ignominiously at the end, was in retrospect quite successful at the core objective of halting inflation – which has since returned with a vengeance.

So neither model of currency union are obvious, for now. Yet, the reasons it may succeed or fail ultimately are not economic, since economics is the servant of politics. The Euro’s greatest weakness has not been economic but political, the Project falling between these two contrasting motivations of democracy and empire. If the Sur starts life with a clearer assertion at the outset, it may have some rationale. The lack of an obvious imperial winner between the two countries, ironically, actually gives the project greater clarity – this will be democratic and complementary, or it will be nothing.

It will probably be nothing, of course. Or, we will quickly discover that Argentina is in such a hole that Brazil effortlessly becomes the imperial power in this relationship. Either way, I await the political will behind this idea to manifest, before I judge the dream quite so harshly, and there remains a lot to learn from the Euro along the way.